Small business loans have been the primary source of external financing for businesses and entrepreneurs for hundreds of years and banks still constitute around 70 percent of all lending supplied to businesses. It’s unsurprising then, that outside of personal funds, a loan from a high street bank is usually the first thing that comes to mind when sourcing finance to start a business or invest into a company’s growth.

Although the bank might have been the first port of call for finance before, times are changing rapidly; banks are approving fewer loans, particularly for small business and business owners are exploring other financing options given the slim chances of approval and the transactional nature of modern business banking relationships.

Bank Approval Rates Diminishing

Historically, a good relationship with your bank might have made the loan application process less formality and paperwork and more about the lender’s perception of your character. Unfortunately, a good character will only take you so far in getting bank finance now.

Although banks recognize the importance of small business to the wider economy, they also have to protect their interests. The world is now fundamentally more risky; natural disasters, worldwide pandemics, faltering supply-chains and now almost unprecedented inflation and rising interest rates all seem to be conspiring against small businesses attempting to get back on their feet post-pandemic.

The small business or more accurately, smaller loan amounts have become a less attractive proposition for big lenders whose underwriting costs are the same whether it’s a $500k or a multi-million dollar loan; combine this profit squeeze with increased risk and years of consolidation and the result is an application process that is subject to far stricter regulation and subsequently, a less than favorable approval rate.

Rates of Small Business Loan Approval

A January article by Forbes states that two years ago, bank approval rates were double what they are today with big banks approving 28.2% of all requests by business and small banks approving 50.6% as at December 2019. In May 2021, the big bank loan approval rate to small business was just 13.5% where alternative lenders’ approval rate was over 24%. Once PPP and other government support concludes, bank approval rates may drop further as the administration fees and backing to these lenders dries up.

Source: Shopify.ca. Accessed: 11.02.2022.

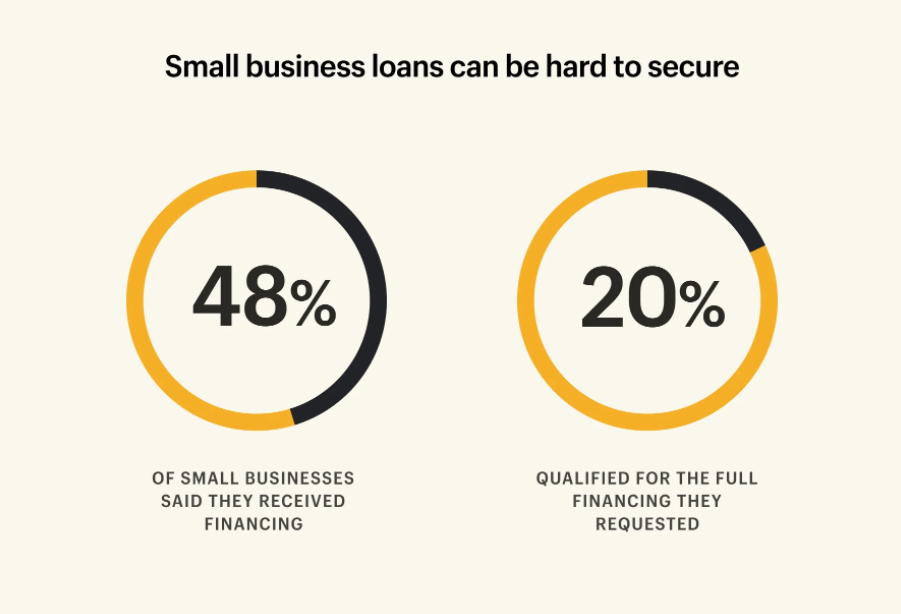

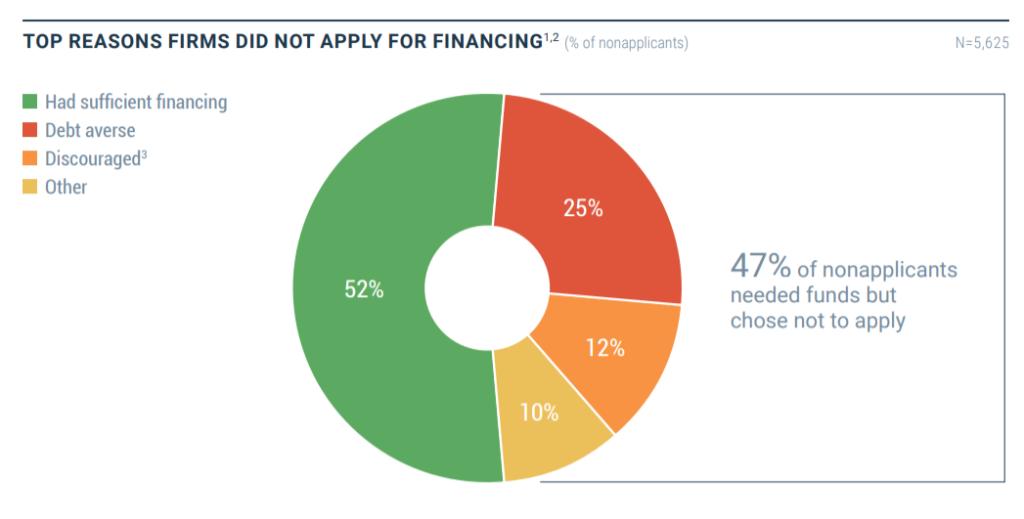

When we look specifically at small businesses, 48% of them reported receiving the finance they applied for and just 20% qualified for the full amount they required. Worryingly, this perhaps tells only part of the story given that 63% of employer firms don’t even take the time to apply for the financing they need according to the 2021 Fed Small Business Credit Survey.

Source: Fed Small Business Credit Survey. Accessed: 11.02.2022.

The top five reasons for the ‘discouraged’ businesses not applying for finance were;

What are the Actual Factors Affecting Small Business Loan Approval?

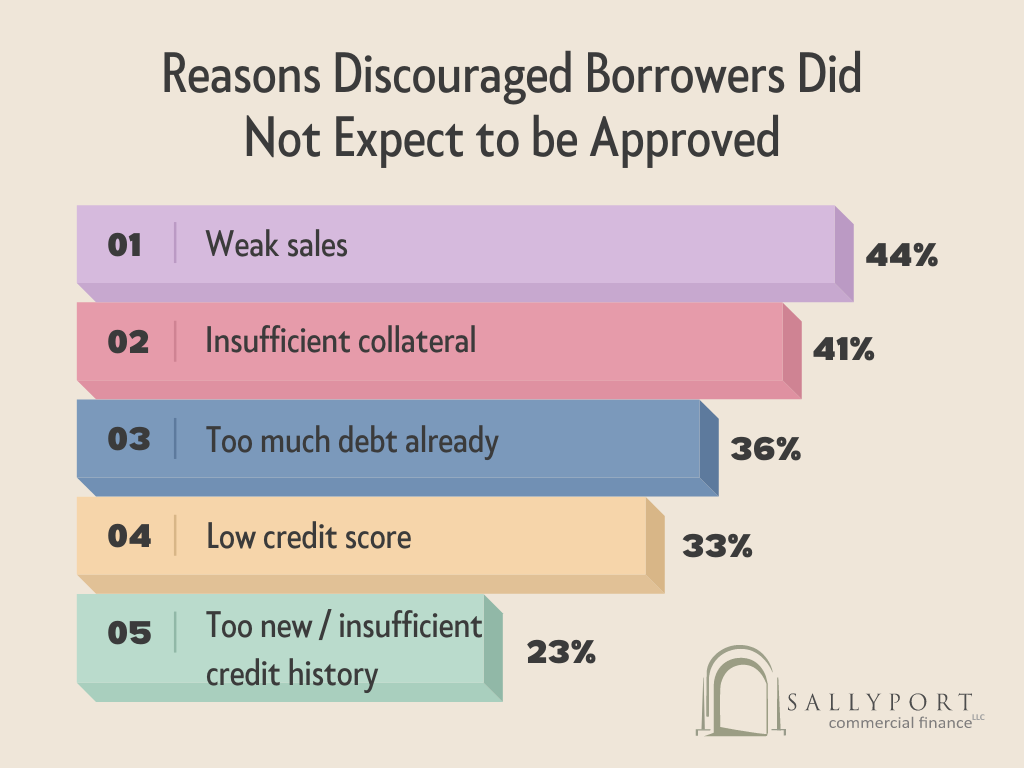

Comparing these perceptions of loan rejection to the actual reasons small businesses were rejected by lenders in 2019, the actual order would be;

- Too much debt – 44%

- Low credit score – 36%

- Insufficient collateral -33%

- Too new / insufficient credit score – 30%

- Weak business performance – 18%

Outside of these factors, there are a multitude of other reasons why it may be difficult to qualify for a small business loan…

- Lack of business management – poor bookkeeping, no solid business plan and missing financial and legal paperwork all signal disorganization to a potential lender.

- Application history – submitting too many loan applications in the hope that one ‘sticks’ can be a red flag for a lender and damage the business’ credit score in the process. If time allows, doing research to identify the type of finance and lender that’s best suited to the business at any given time will be time well spent.

- Attitude is everything – especially at a time when lenders are getting pickier, being prepared with all the documentation they’ll need to see and demonstrating confidence and enthusiasm for the business’ future can still make a big impression.

Ultimately, underlying every decision however will be the company’s cash flow situation. If we delve further into the reasons for rejection, there is a concerning picture emerging for businesses cash flow and their ability to access low-cost loans.

Companies have more debt than ever. Canadian businesses not only have CEBA loan repayments on the horizon before the year is out but have taken on an average of $170,000 in debt during the pandemic. Approximately a fifth (20.6%) of businesses with 1-19 employees report that they don’t have the ability to take on more debt.

Whilst figures are not as accessible for American small businesses, it’s clear that they’re facing similar problems to their Northern neighbors with 41% saying that their increased debt load could undermine their financial stability this year. With 44% of U.S. small businesses having less than three months of cash reserves, finance may be very hard to come by.

Rising costs across the board and a weak outlook for sales performance amplify the need for small business owners to enhance cash flow management and where necessary, work with external professionals on sensible financial solutions that will lead them to recovery.

Closing the ‘Capital Gap’

The landscape of the small business lending market feels very similar to the period following the 2008 financial crisis when banks started to contract lending at a time when businesses had to take on more debt for their very survival – history now appears to be repeating itself as a result of an altogether different crisis.

The reliance of small businesses on traditional finance and their vulnerability to increasingly volatile conditions in bank lending has highlighted the need for alternative finance sources to bridge capital gaps. In previous financial crises, the number of startups entering the market has declined but the last couple of years has created entrepreneurs unlike the fallout of any normal downturn; these entrepreneurs and small businesses have always been and will continue to be the lifeblood of the economy and flexible, timely financial solutions are required to ensure their success.

Alternative lenders are seizing the opportunity to provide tenacious small business owners with a range of financial products to meet their needs along with the relationship-based service that they’ve come to enjoy. Poor cash flow needn’t be a barrier to securing finance with an alternative lender, however planning ahead is key to success.

As we go through challenging trading conditions in 2022, the Sallyport team are always here to discuss tailored working capital solutions for your new or existing business, reach out today.

How SMEs Are Planning for Growth in 2026 (Despite Uncertainty)

Small and medium-sized enterprises (SMEs) across North America entered 2026 with a clear understanding: uncertainty is not going away, but…

Read More

What are the Biggest Risks to Business in 2021 and Beyond

If this was asked at this point last year, the response would be in major contrast as to the biggest…

Read More

AG Machining Client Testimonial

AG Machining Client Testimonial

View Now

The Most Financial Time of the Year

Sallyport commercial finance’s Annual Holiday Music Video!

View Now