Businesses experience cash flow challenges for a number of reasons. These problems are not all bad news; a company may be growing so fast for example, that a short-term need arises for additional working capital and existing credit lines won’t stretch far enough. These funds take the strain off cash flow and can help with big purchases, securing volume discounts or investment in workforce and payroll expansion while waiting for payments from clients to materialize.

A cash flow loan is just one of the options available to you in this scenario and as a form of debt finance, won’t require you to surrender equity.

What are Cash Flow Based Loans?

Unlike a conventional bank loan, for which businesses will be subject to a thorough credit analysis, a cash flow loan is a type of unsecured borrowing that is based upon the lender’s perception of the business’ ability to generate future cash flow. In essence, a cash flow loan allows you to borrow against future revenue.

Because lenders are primarily concerned with past cash flow performance along with projections, the factors used to assess businesses for a traditional loan are much less important to them and in this way, a cash flow loan can be more accessible to many entrepreneurs. Businesses which are relatively new, have limited assets to use as collateral for a loan or have a less than average credit rating can all be great candidates for cash flow lending, as are high growth companies who are utilizing all of their available credit but need capital for investment.

How is a Cash Flow Loan Different from a Standard Business Loan?

Aside from the less stringent qualification criteria for a cash flow loan, there are some other key differences worth noting between a cash flow loan and a conventional business loan, namely that lending on a conventional basis typically involves a business’ assets or even the personal assets of the business owner being used as collateral for the loan.

All lenders assume a level of risk when funding a company, however collateral-based lenders will mitigate their risk by assessing the value of a business’ assets and be able to use those to recoup their losses in the event a business can’t make their repayments. Those assets can include both commercial assets by way of real estate and equipment and personal investments, bank accounts and residential property.

As future performance of the business is the foundation for a cash flow loan, success for the borrower ultimately corresponds with success for the lender too. There’s an argument therefore that cash flow lenders are more heavily invested in the success of the business and its management in order to protect their interests; many cash flow lenders utilize a professional network of SME consultants whose knowledge and experience can be tapped into to support the business through challenging periods.

How Can a Cash Flow Loan Benefit Growing SMEs?

Although rapid growth is an enviable position to be in, it can also be a frustrating time for business owners without a big cash reserve. The faster the growth, oftentimes the bigger the cash flow problems get.

Some of the signs that a growing business may need to consider a cash flow loan are…

- You’re introducing new products but sales growth will take longer than the costs of investment into manufacturing, equipment, new hires or marketing;

- You’ve got one or two large customers (high customer concentration), with extended credit terms, who pay far later than your costs of production are incurred;

- You have too many clients to whom you’ve extended payment terms and before you know it, you can’t meet your monthly payables;

- You need to purchase inventory or raw materials and take advantage of volume discounts;

- Purchase orders are growing exponentially but your capital capability is lacking. In the worst case scenario, a business using overseas suppliers may have a 180-day sales cycle before their receivables come in; production and operational expenses however still need to be paid monthly in most cases.

Many of these challenges can go unnoticed as you focus on revenue building, but getting ahead of the curve will help you to secure cash flow finance quickly when you need to invest.

What do Lenders Look at for a Cash Flow Loan?

Lenders will be looking at how healthy your cash flow is and want to understand the business model in some detail to form a view on the cash needs of the business. Depending on the company, they might use all or some of these elements to determine suitability…

- Quality of Accounts Receivable;

- Accounts Payable Performance and Process;

- Business Plans;

- Sales Forecast;

- Financial Statements; Profit and Loss (P&L) or Income Statement, Balance Sheet, Cash Flow Statement;

- Growth Capital Requirements.

Each business will be assessed for a cash flow loan on its own merits and each lender’s processes will be different. It’s important to bear in mind that time in business, credit rating and past performance need not prevent you from applying as lenders will be more interested in your potential.

The cash flow forecast (also referred to as cash flow statement) will be one of the most important documents for lenders to see when assessing creditworthiness for a cash flow loan.

How to Prepare a Cash Flow Forecast for a Business Loan

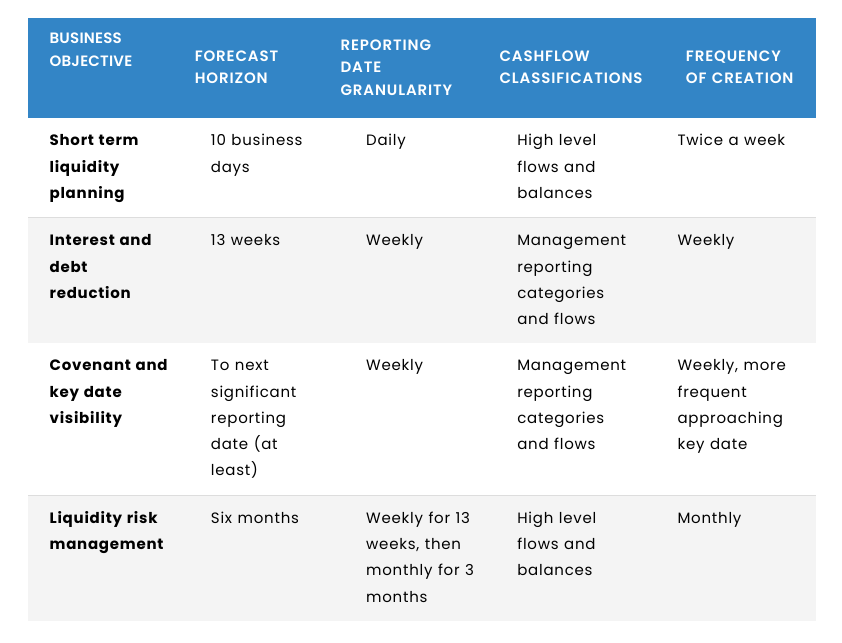

There isn’t a one-size-fits-all to cash flow statements. A forecast can take many forms, it really depends on what the business objectives are and what you want to use the document for but for most businesses a combination of daily, monthly and yearly forecasting would cover a number of business objectives as outlined by software company ‘Cash Analytics’ here…

Although yearly forecasts are helpful for long-term growth planning and capital projects, newer businesses don’t always have a long period of actuals to record but an accurate and realistic forecast is a great start.

A simple cash flow statement needs to include all incoming and outgoing cash for the business and subcategories within each. Income details should document all cash earned through sales, accounts receivable, investments and financing and a breakdown of expenses will include items such as bills, operational costs, asset purchases and the servicing of debt payments.

There are many free business resources available for download online such as this cash flow projection template from Microsoft. If you’re at all uncertain about how to create or interpret a cash flow forecast however, we’d always recommend consulting an experienced accountant or financial advisor.

Need More Insight on Business Cash Flow Loans?

Cash flow and business growth usually go hand-in-hand, you can’t have one without the other. To get further information on the pros and cons of a cash flow loan for your business, reach out to our team today and we can guide you through all the options open to you.

A loan can also be used in combination with other financial products, should a more bespoke package fit the needs of your unique circumstances. Whatever your business finance needs, we look forward to supporting you in the next stage of your business’ growth.

Meet Ingrid Chen – Sallyport Senior Account Executive

Meet Ingrid Chen – Finance Professional with over 30 Years’ Experience Ingrid has spent 27 years in the factoring and…

Read More

A to Z of Small Business Finance and Credit Terms

Most small business owners go into business to follow a passion or create freedom in their career and lives. It’s…

Read More

American Business Women’s Day

Sallyport Commercial Finance Celebrates American Business Women’s Day

View Now